I wrote for Naavik about Monopoly Go’s disclosed performance metrics and what they reveal about the game’s underlying economics. Read the full article here.

Why I wrote about this

Sometimes companies share just a bit more than they mean. With Scopely sharing revenue, downloads, DAU, and even marketing paybacks, it was too good an opportunity not to break down what the business actually looks like under the hood.

The gist of it

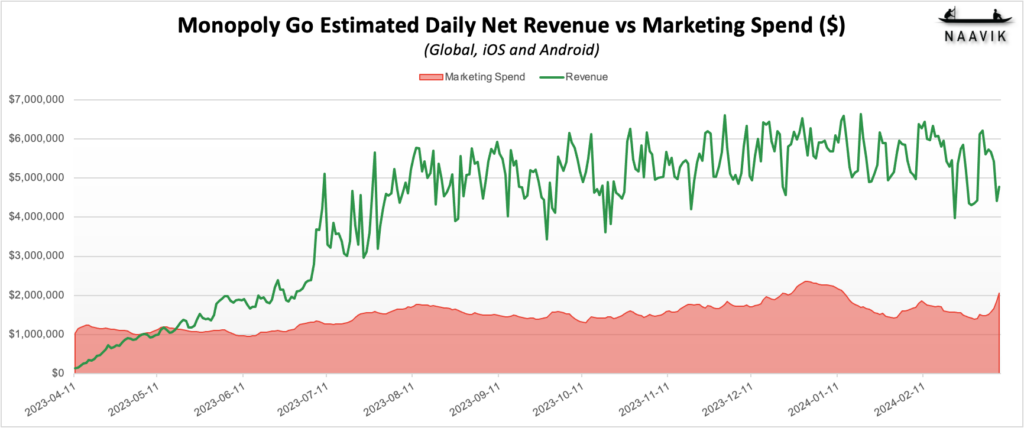

Scopely revealed that Monopoly Go has surpassed $2B in lifetime gross revenue on 150M downloads, supported by less than $500M in bought media and over 10M daily active users. Combined with disclosed payback windows (“measured in weeks” early on and now around 120 days), these figures provide enough anchors to model the game’s business with reasonable confidence.

The implied blended eCPI lands around $3.3. Even allowing for a steady increase over time, that’s extraordinarily efficient at this scale, particularly for a social casino-adjacent title competing in high-value geos. Few games at the top of the grossing charts manage to acquire users this cheaply without sacrificing cohort quality.

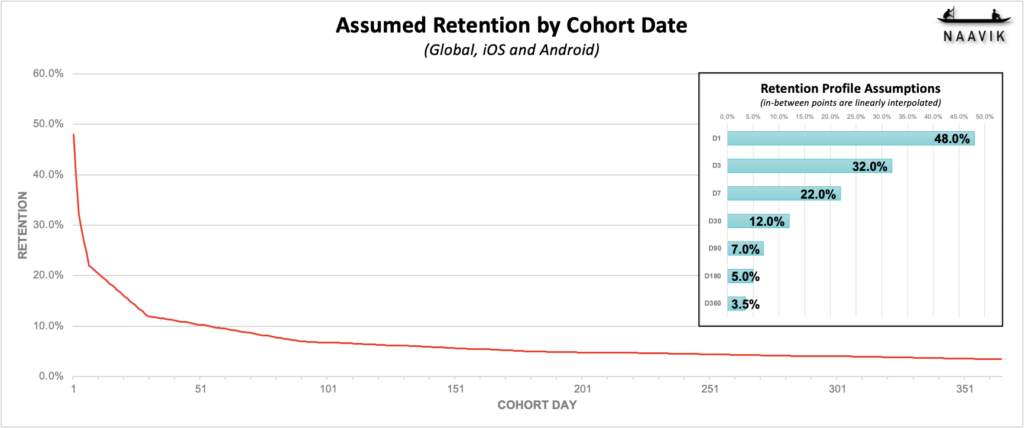

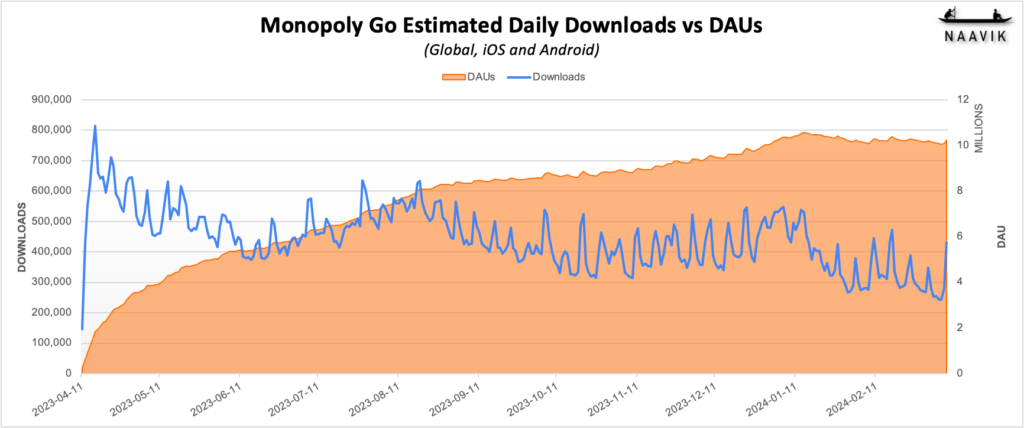

Combining the DAU disclosure with data.ai download data, we can reverse-engineer retention assumptions that resemble a strong but fairly standard casual game profile.

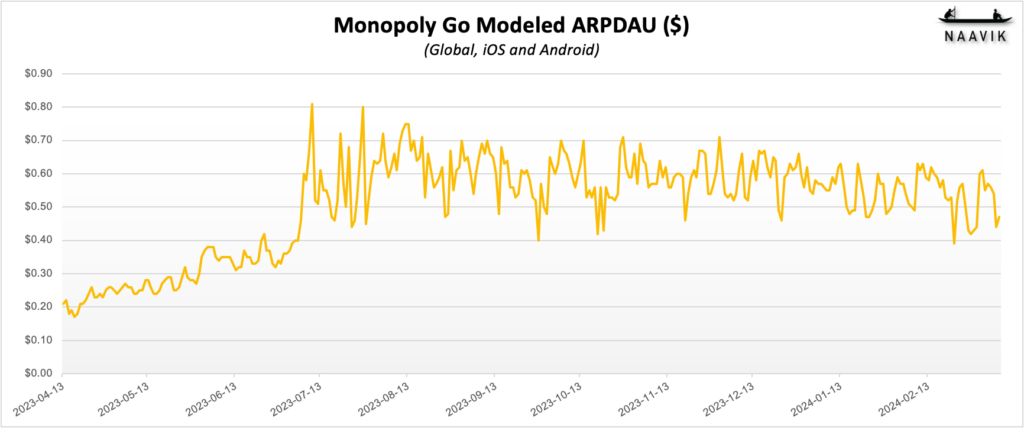

Finally, when paired with roughly $6M in daily net revenue, we can model ARPDAU, which sits at around $0.50 globally. This is high for casual, but fully plausible within the social casino space.

Where things get interesting is growth. After a blistering first six months, downloads have cooled and revenue has stabilized. DAU appears flat to slightly declining. The high-growth phase seems to be over, at least for now. That raises the key question: if paybacks are still within 120 days, why isn’t marketing spend accelerating further? The most likely explanation is rising CPIs and weakening marginal cohorts at scale. Monopoly Go’s extraordinary early economics were powered by a rare combination of IP-driven distribution advantage and excellent product execution. Whether it can sustain momentum from here depends less on the initial breakout and more on disciplined live operations and UA optimization.

Key takeaways

- $2B lifetime gross revenue on 150M installs implies near-perfect execution.

- ~10M DAU and ~$0.50 ARPDAU make for a very robust free-to-play engine.

- Sub-$5 effective CPI at scale is the game’s true superpower.

- Even if growth has slowed, Monopoly Go is already on track to join mobile’s long-term classics.